What if you could make that late fee disappear?

If you usually pay on time, contact the company and ask whether it will remove the charge as a one-time courtesy. Credit card issuers, banks, landlords, lenders, utilities, and service providers may sometimes waive a fee, although they are not required to do so.

Call as soon as you notice the charge. Be polite, brief, and specific:

“I have normally kept this account in good standing, but I missed the due date this month. I have now made the payment. Would you please remove the late fee as a one-time courtesy?”

You can also explain a genuine reason, such as a paycheck delay, medical problem, billing error, or automatic-payment failure. You do not need to tell your entire life story.

If the first representative says no, ask whether a supervisor or account specialist can review the request. Remain calm. A fee waiver is more likely when you are respectful and have a strong payment history.

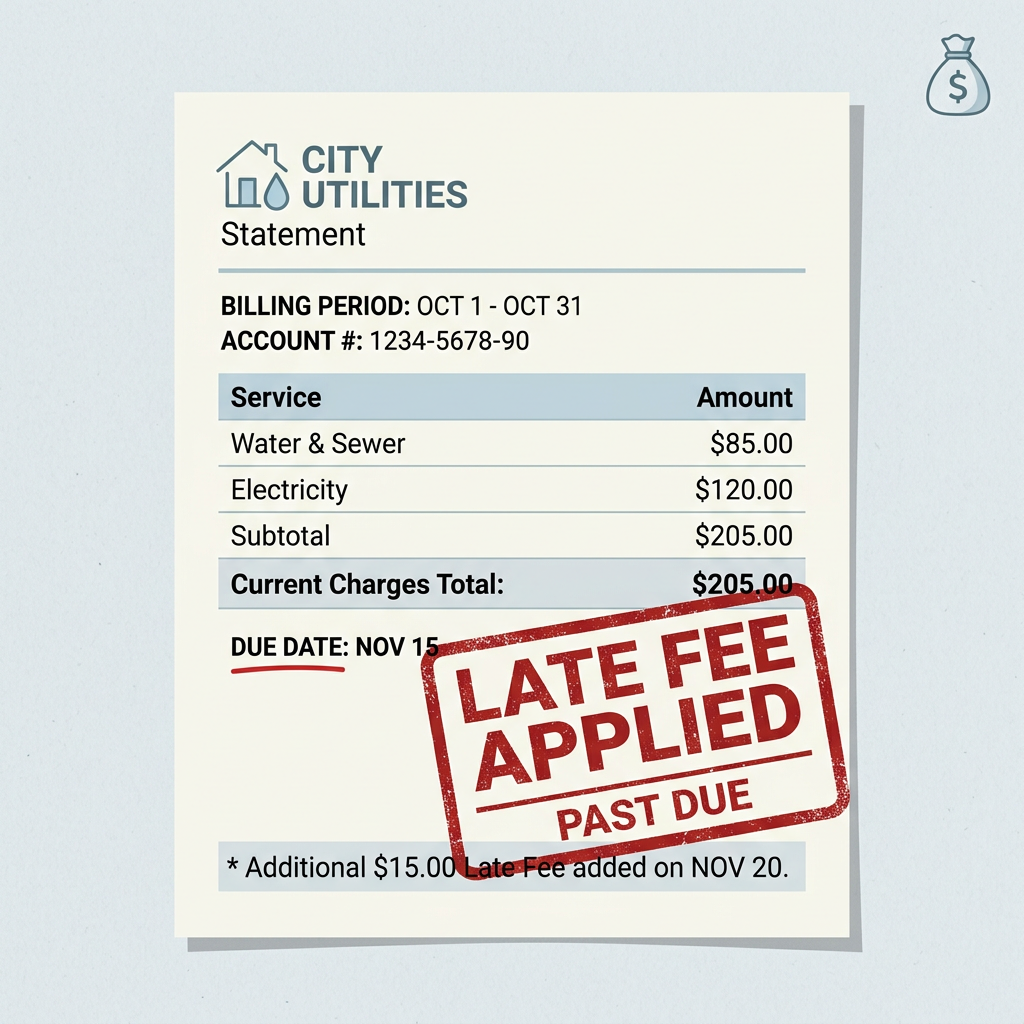

Suppose a credit card charged a $30 late fee and your utility charged $15. Getting both reversed would save $45—the equivalent of several meals or part of a tank of gas.

After the call, fix the cause of the problem. You might change the due date, set a calendar reminder, enable a low-balance alert, or schedule the minimum payment automatically.

Be careful with autopay if your account balance is unpredictable. Avoiding a late fee is not helpful if the automatic withdrawal causes an overdraft.

Ask whether the late payment will be reported to a credit bureau, but understand that removing a fee does not necessarily change credit reporting.

You may not succeed every time. Still, a five-minute phone call can produce one of the best hourly returns available: keeping money that would otherwise disappear into a fee.